True Cost of Homeownership in 2026: Mortgage, Taxes, Insurance, HOA, Maintenance and Repairs

A full monthly homeownership cost framework that goes beyond the mortgage payment.

The mortgage payment is not the true cost of owning a home. It is only the most visible part. A buyer who can afford principal and interest may still be stretched by property taxes, insurance, HOA dues, utilities, repairs, and maintenance.

In 2026, this matters more than ever because affordability is not just about the purchase price. Mortgage rates, insurance premiums, property taxes, repair costs, and local fees can turn two homes with the same price into very different financial decisions.

Quick answer

The true monthly cost of homeownership equals principal and interest plus property taxes, homeowners insurance, HOA dues, PMI if applicable, utilities, maintenance reserve, repair reserve, and any location-specific fees or assessments. Buyers should calculate this full number before deciding whether a home is affordable.

A home that looks affordable at $3,200 per month may actually cost $4,500 to $5,500 per month once the full cost is included.

The homeownership cost formula

Use this formula before you make an offer:

True monthly ownership cost = principal and interest + property taxes + homeowners insurance + HOA dues + PMI + utilities + maintenance reserve + repair reserve + other required housing costs.

The formula looks simple, but many buyers skip two or three categories. That is where surprises happen.

| Cost category | Include it because |

|---|---|

| Principal and interest | The base loan payment |

| Property taxes | Local taxes can be high and may rise after purchase |

| Homeowners insurance | Premiums vary by risk, location, coverage, and replacement cost |

| HOA dues | Monthly dues can change and special assessments can appear |

| PMI | Required for many lower-down-payment loans |

| Utilities | Electricity, gas, water, sewer, trash, and internet add up |

| Maintenance | Routine upkeep prevents larger problems |

| Repairs | Major systems eventually fail |

| Other costs | Pest control, landscaping, security, flood insurance, local fees |

The U.S. Census and ACS housing-cost framework also treats housing cost as more than the mortgage alone. A realistic affordability analysis should do the same.

Why mortgage calculators understate the real number

Many online calculators show principal and interest first. Some include estimated taxes and insurance. Fewer include maintenance, repairs, utilities, HOA risk, insurance inflation, or planned improvements.

That creates a dangerous mental shortcut. Buyers begin with the lowest number and emotionally commit to the house. Then they discover the full payment during underwriting, inspection, or the first year of ownership.

A better process is to start with the full number from day one. If the home still works, you can move forward with more confidence.

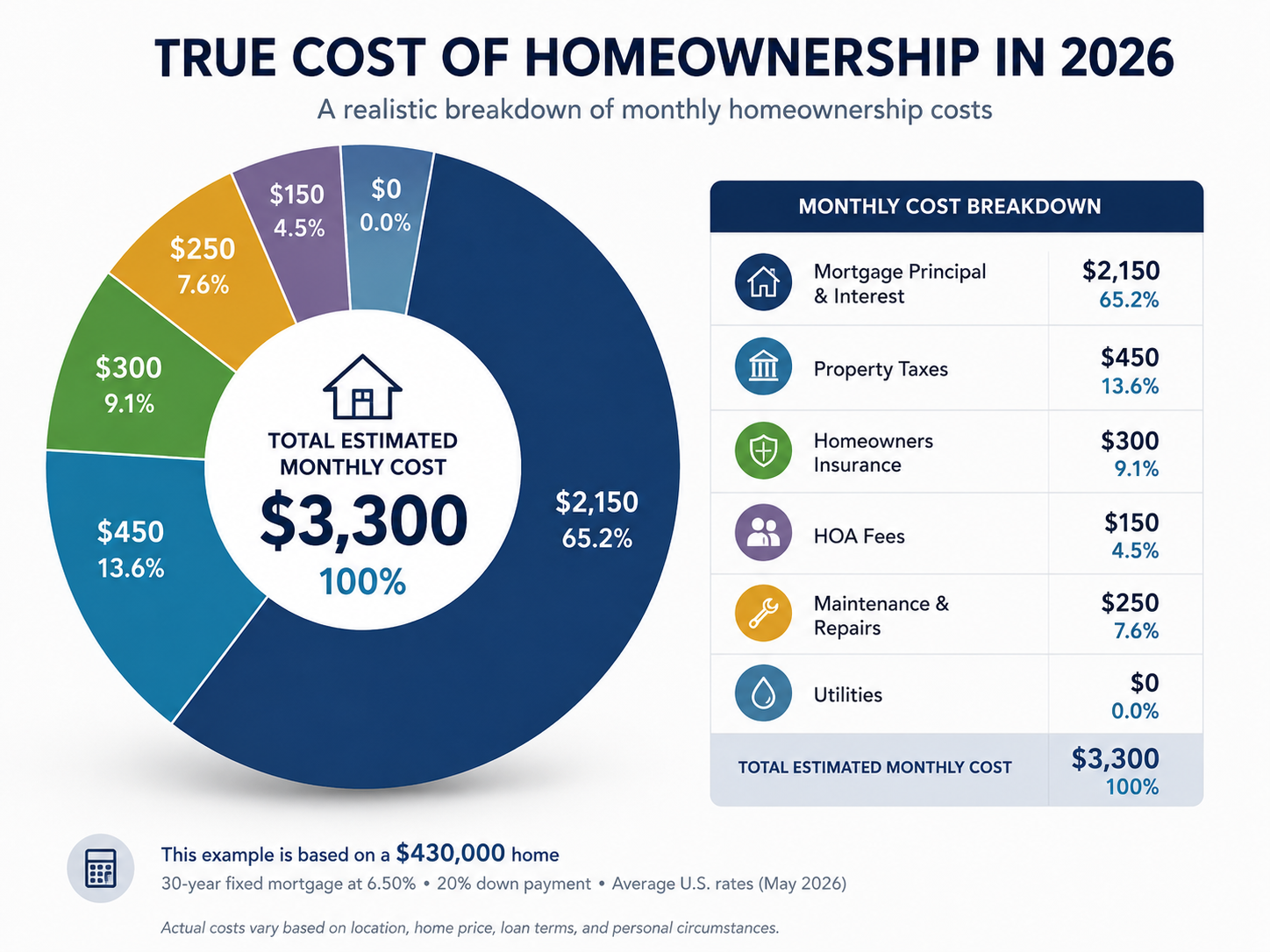

Example: $625,000 home with a 20% down payment

Assume a buyer is considering a $625,000 home with 20% down. The loan amount is $500,000. Using a 30-year fixed-rate assumption near 6.52%, the principal and interest payment is about $3,167 per month.

That is not the full cost.

| Item | Example monthly amount |

|---|---|

| Principal and interest | $3,167 |

| Property taxes | $650 |

| Homeowners insurance | $225 |

| HOA dues | $150 |

| Utilities | $350 |

| Maintenance reserve | $520 |

| Repair reserve | $250 |

| Estimated true monthly cost | $5,312 |

The buyer may have thought this was a $3,167 decision. It is closer to a $5,312 monthly ownership decision.

That does not mean the home is unaffordable for everyone. It means the decision should be made using the real number.

Principal is not the same as cost

Principal repayment is different from interest, taxes, insurance, and repairs. Principal builds equity. Interest and operating costs do not.

That distinction matters when comparing buying to renting. A $3,167 mortgage payment is not all “lost money.” Part of it is principal that reduces the loan balance. But a buyer still needs cash every month to make the full payment. Home Decision Lab separates cash flow from long-term wealth because both matter.

A homeowner can be building equity and still be cash-flow stressed. A renter can avoid repair risk and invest the difference. The right comparison looks at both monthly affordability and net worth over time.

The costs buyers most often underestimate

Homeowners insurance

Insurance can vary widely by state, zip code, property age, roof type, wildfire risk, wind risk, flood risk, claims history, and replacement cost. Do not rely only on a generic estimate. Ask for a quote early.

Property taxes

The seller’s tax bill may not be your future tax bill. Some areas reassess after sale. New construction, supplemental assessments, school bonds, and local districts can change the amount.

HOA dues and special assessments

An HOA fee is not just a monthly number. Review the budget, reserves, meeting minutes, pending litigation, insurance coverage, and special assessment history. A low HOA with weak reserves can be riskier than a higher HOA with healthy reserves.

Maintenance and repairs

Maintenance is not optional. Roofs, HVAC systems, water heaters, plumbing, electrical panels, exterior paint, appliances, fences, decks, and drainage systems all age. A newer home may have lower near-term risk, but no home has zero maintenance.

Utilities

A larger home, older windows, poor insulation, electric heat, a pool, irrigation, or extreme climate can change the monthly cost dramatically.

How to estimate maintenance without pretending you know the future

Use three layers:

1. Routine maintenance: landscaping, filters, gutter cleaning, pest control, small repairs. 2. System replacement reserve: roof, HVAC, water heater, appliances, paint, flooring. 3. Inspection adjustment: increase or decrease the reserve based on actual condition.

A common starting point is 1% of home value per year, but this is only a rough rule. A $700,000 home does not automatically need $7,000 of maintenance every year, but it may need much more if major systems are old. A cheaper older home can cost more to maintain than a newer expensive home.

How true cost changes the rent-vs-buy decision

Rent is usually easier to understand because it is one monthly number. Ownership is a bundle of costs, risks, and potential equity.

When comparing rent and buy, do not simply compare rent to mortgage principal and interest. Compare rent to the non-equity cost of ownership, then separately compare long-term net worth.

The non-equity ownership cost includes interest, taxes, insurance, HOA, maintenance, repairs, and transaction costs. Principal paydown and down payment are wealth transfers, not pure expenses. This distinction is the difference between a shallow calculator and a useful decision model.

Decision rules for buyers

Use the full payment before you tour seriously

If a home fails your full monthly cost test, touring can create pressure to rationalize the numbers later.

Keep a repair reserve after closing

A buyer who uses every dollar for the down payment and closing costs may be exposed even if the monthly payment works.

Stress test the payment

Ask what happens if insurance rises 20%, HOA dues rise 10%, or the first-year repairs are higher than expected.

Compare two homes by full cost, not price

A $650,000 home with high taxes and old systems may cost more than a $700,000 home with lower operating risk.

How Home Decision Lab helps

Use Home Decision Lab’s Home Analysis Report at Home Analysis Report to compare the full monthly cost of a specific home. If you are also deciding whether to keep renting, use Rent vs Buy calculator to compare ownership cost, rent, opportunity cost, and net worth over time.

FAQ

What is included in the true cost of homeownership?

The true cost includes principal and interest, property taxes, insurance, HOA dues, PMI, utilities, maintenance, repairs, and any required fees or assessments.

Is mortgage principal a cost?

Principal is a cash payment, but it is not the same as interest or taxes because it reduces your loan balance and builds equity. You still need to afford the cash flow, but long-term wealth analysis should treat principal differently from true expenses.

How much should I budget for repairs after buying a house?

Start with a maintenance reserve, then adjust based on inspection findings, age of roof, HVAC, plumbing, electrical systems, appliances, drainage, and exterior condition.

Why is homeowners insurance so important in affordability?

Insurance can change the monthly payment and may rise over time. It is especially important in areas with wildfire, wind, hail, flood, or high replacement-cost risk.

Should I use the seller’s property tax amount?

Use it only as a starting point. Your tax bill may change after purchase depending on local assessment rules, exemptions, purchase price, and local tax rates.

What is the biggest mistake buyers make with monthly cost?

The biggest mistake is comparing rent to principal and interest only. That leaves out several ownership costs and can make buying look cheaper than it really is.

Data sources and assumptions used in this article

This article is educational and uses public market context plus example calculations. Numbers should be refreshed before publishing if Home Decision Lab has newer internal data.

- Freddie Mac Primary Mortgage Market Survey context: 30-year fixed-rate mortgage averaged 6.52% for the week reported June 11, 2026.

- FHFA House Price Index context: U.S. home prices were up 1.7% year over year in Q1 2026 and up 0.5% from Q4 2025.

- U.S. Census/ACS housing-cost framing: ownership cost includes more than the mortgage payment, including taxes, insurance, utilities, fees, and other required housing expenses.

- RentCast can be used for static data snapshots where available: rent estimates, value estimates, comps, property records, listings, and local market trend data. Do not expose an API key in public blog code.

Source URLs:

- https://www.globenewswire.com/news-release/2026/06/11/3310694/0/en/Mortgage-Rates-Average-6-52.html

- https://www.fhfa.gov/reports/house-price-index/2026/Q1

- https://www.census.gov/acs/www/about/why-we-ask-each-question/housing/

- https://www.census.gov/newsroom/press-releases/2025/acs-5-year-estimates.html

- https://developers.rentcast.io/reference/rent-estimate-long-term

- https://www.rentcast.io/api

Educational disclaimer

Home Decision Lab is an educational decision-support tool, not a lender, real estate broker, tax advisor, or financial advisor. This article should not be treated as personal financial, legal, lending, investment, or tax advice. Buyers and homeowners should confirm numbers with qualified professionals before making an offer, refinancing, selling, renting, or moving.

Educational only. This is not financial, legal, tax, mortgage, investment, or real estate advice.